What Are the 7 Tax-Free Investments in Australia? Superannuation, Bonds & More

Maximizing Returns: Tax-Efficient Investment Options in Australia

In Australia, several tax-efficient and tax-free investment options are available to maximize returns and minimize tax liabilities:

Superannuation (Super) is one of the most tax-effective investments, with contributions taxed at 15% and earnings taxed at 15% on income and 10% on capital gains. Withdrawals after age 60 are generally tax-free, making it ideal for long-term retirement savings.

Investment Bonds offer a tax-effective alternative to traditional investments, taxed internally at 30%. After 10 years, earnings become tax-free.

Negatively Geared Properties allow investors to deduct property-related expenses from taxable income, reducing tax liabilities while aiming for long-term capital growth.

Early Stage Innovation Companies (ESICs) provide tax exemptions on capital gains for shares held over a year, plus a 20% tax offset for qualifying investments.

ETFs and Shares offering franked dividends are popular, as franking credits can reduce or eliminate taxes on dividend income, particularly for those with a 30% marginal tax rate.

What Are the 7 Tax-Free Investments in Australia?

Australia’s investment landscape offers a range of opportunities that can help investors grow their wealth without hefty tax implications. Understanding tax-free investments is crucial, especially for those looking to maximise their returns without sharing a significant portion with the government.

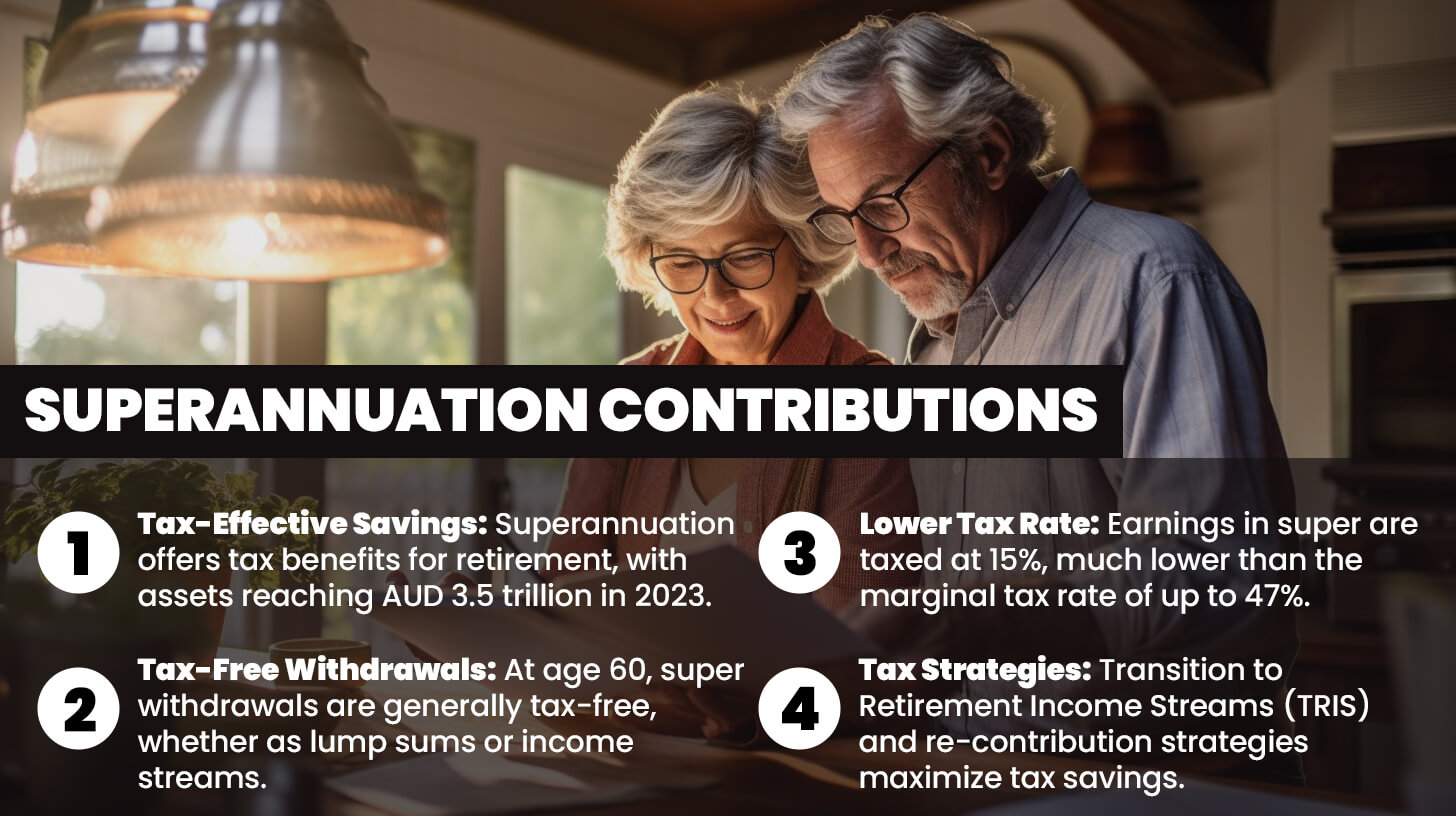

Superannuation Contributions

Superannuation is a tax-effective investment strategy essential for Australians planning for retirement.

According to the Australian Taxation Office (ATO), superannuation assets reached approximately AUD 3.5 trillion as of 2023, highlighting its popularity among Australians.

Super offers unique tax benefits, especially once investors reach the pension phase at age 60. At this point, withdrawals, whether lump sums or income streams, are generally tax-free.

For instance, consider an individual who contributes AUD 25,000 annually into their super fund over 30 years. Assuming an average annual return of 7%, their balance could reach over AUD 2 million by the time they retire.

During the accumulation phase, the earnings are taxed at a concessional rate of 15%, significantly lower than the marginal tax rates that can reach up to 47% for high-income earners.

Once the individual retires and transitions into the pension phase, withdrawals become tax-free, allowing them to enjoy their savings without the usual tax burden.

In addition, making after-tax (non-concessional) contributions up to AUD 110,000 per year, or AUD 330,000 over three years using the bring-forward rule, can further enhance the super balance.

These contributions grow within the fund without being taxed, creating a potent tax-free growth environment.

Superannuation strategies like transitioning to retirement income streams (TRIS) and re-contribution strategies further amplify tax savings, especially for those aiming to reduce taxable estate values or manage tax liabilities effectively.

Australian Government Bonds

Australian Government Bonds (AGBs) have long been a staple for conservative investors seeking stability and predictable returns. These bonds are not completely tax-free, but they provide specific exemptions that make them highly attractive in a diversified portfolio.

Infrastructure bonds, for example, are sometimes issued with tax concessions, including interest payments exempt from certain taxes.

According to the Reserve Bank of Australia (RBA), AGBs accounted for AUD 800 billion in market value by 2023, reflecting their substantial role in the national financial ecosystem.

A detailed example includes Treasury Indexed Bonds, which offer inflation-linked returns. The principal increases with inflation, and interest payments are calculated on this adjusted principal amount, providing real protection against inflation.

Some of these bonds have specific tax treatments that allow investors to benefit from tax-free capital gains under certain conditions.

Investors who purchased AUD 100,000 worth of AGBs yielding 3% annually and held them for 10 years could see a return of AUD 130,000, depending on the specific type of bond and its conditions.

With infrastructure bonds, investors can earn interest that may be partially or fully exempt from tax, depending on the bond’s structure and government incentives aimed at promoting infrastructure development.

For high-net-worth individuals, these bonds offer a secure way to maintain capital while benefiting from reduced tax exposure, making them an intelligent choice for low-risk, tax-efficient investing.

Tax-Free Investment Bonds

Investment bonds offer a unique tax structure that appeals to long-term investors. These financial instruments are taxed internally at the company rate of 30%, and if held for at least 10 years, withdrawals become tax-free.

According to a study by Rainmaker Information, investment bonds have grown in popularity, with the market seeing a 15% increase in new inflows annually over the past five years.

A practical example is investing in an investment bond with an initial capital of AUD 50,000 and making annual contributions of AUD 10,000 for 10 years. Assuming a 6% return per annum, the bond’s value could grow to approximately AUD 176,000 by the end of the 10-year period.

During this time, investors do not need to declare the bond’s earnings on their annual tax returns, simplifying tax reporting and ensuring that the investment grows without additional tax obligations.

Investment bonds are particularly useful for estate planning as they allow for tax-free transfers to beneficiaries, bypassing the complexities and taxes often associated with traditional inheritances.

For example, a parent investing in a bond for their child’s future education costs can enjoy 10 years of tax-free growth, providing a financial head start without the burden of annual tax assessments.

This strategic use of investment bonds makes them a powerful tool for those seeking to manage wealth and tax liabilities effectively.

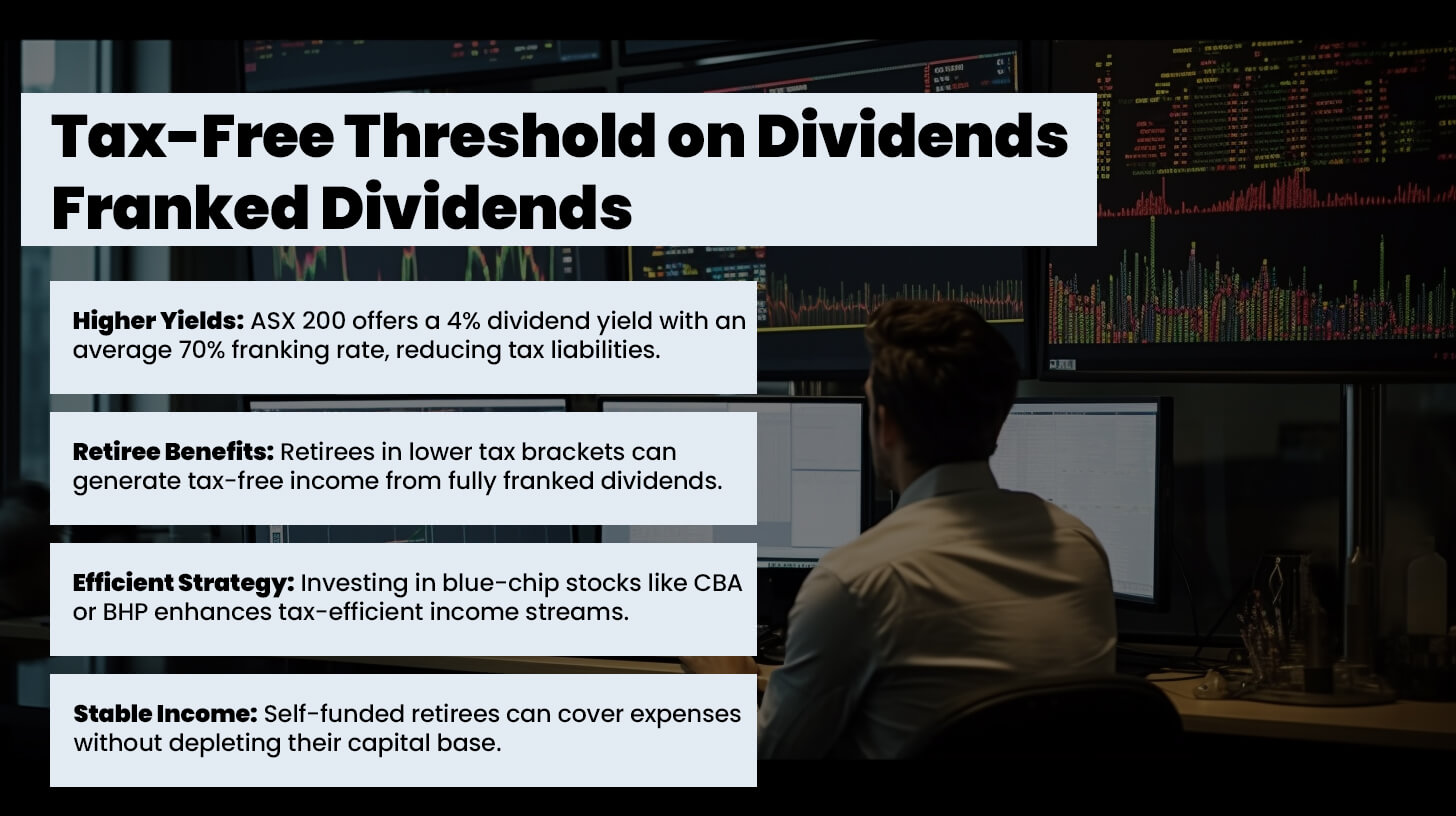

Tax-Free Threshold on Dividends – Franked Dividends

Franked dividends represent a unique opportunity within the Australian tax system, especially when compared to international counterparts where double taxation on corporate profits and dividends is common.

As of 2023, the ASX 200 had a dividend yield of around 4%, with an average franking rate of 70%. This means that for many companies, a significant portion of the dividend income is backed by franking credits, which can offset personal tax liabilities.

For instance, if an investor receives AUD 5,000 in fully franked dividends, the attached franking credits might be worth an additional AUD 2,143, representing tax already paid by the company at a 30% rate.

If the investor’s marginal tax rate is below 30%, they could receive a tax refund on the difference, effectively making the dividends tax-free.

This system is especially beneficial for retirees in the zero or low marginal tax brackets, allowing them to generate tax-free income streams that enhance their standard of living.

A detailed example involves investing AUD 100,000 in blue-chip stocks like Commonwealth Bank or BHP, known for consistently paying fully franked dividends. Over a year, this investment might yield AUD 4,000 in dividends plus associated franking credits.

For investors who strategically manage their income streams, these franking credits can result in tax refunds, turning their portfolio into a highly tax-efficient income generator.

This strategy is particularly advantageous for self-funded retirees who can use these dividends to cover living expenses without drawing down their capital base.

Capital Gains Tax (CGT) Exemptions

Australia’s Capital Gains Tax exemptions provide substantial opportunities for investors to reduce their tax liabilities significantly.

The most widely known exemption is for the sale of one’s primary residence. According to CoreLogic, the median house price in Sydney has grown by an average of 6.8% annually over the last 20 years.

For homeowners, this equates to substantial capital gains, which, if realised upon selling their principal home, are entirely exempt from CGT.

A notable example involves a property purchased in 2000 for AUD 400,000 and sold in 2023 for AUD 1.5 million. Without the primary residence exemption, the CGT liability could be upwards of AUD 330,000, assuming a top marginal tax rate and 50% CGT discount.

However, this exemption allows homeowners to retain the full profit without paying a cent in tax, making property ownership not only a path to security but also a powerful tax-free wealth-building strategy.

Small business CGT concessions provide additional avenues for tax-free growth. The 15-year exemption allows business owners who have held their business for 15 years and are over 55 to sell their business tax-free upon retirement.

For instance, a business owner selling a small café for AUD 800,000 after 15 years of operation can pocket the entire amount tax-free, provided they meet the eligibility criteria.

These exemptions serve as a significant incentive for entrepreneurs, rewarding long-term investment in their ventures.

Tax-Free Accounts for Minors

Minor investment accounts are designed to encourage saving from an early age, providing significant tax benefits.

According to the ATO, minors’ income is taxed at specific rates, with the first AUD 416 generally tax-free, and earnings between AUD 417 and AUD 1,307 taxed at 66%, before reverting to standard adult rates for earnings above this threshold.

While the tax rates can be punitive to discourage income shifting, structured minor accounts that stay within the lower thresholds can grow tax-free or at very low tax rates.

An example includes setting up a high-interest savings account for a child, contributing AUD 1,000 annually at an interest rate of 3%. Over 10 years, this could grow to around AUD 11,000, with the majority of the interest income falling below the taxable threshold, resulting in minimal or no tax liability.

Additionally, structured investment funds designed for minors allow parents to contribute in a controlled manner, ensuring that income stays within tax-free or low-tax thresholds, facilitating effective wealth transfer and growth.

These accounts also teach valuable financial skills, helping children understand the benefits of saving and investing early in life. Moreover, funds in these accounts can be earmarked for significant future expenses, such as education or a first home deposit, leveraging compounding returns over many years.

The strategic use of minor investment accounts blends financial education with tax efficiency, making them a versatile option for building a child’s financial future.

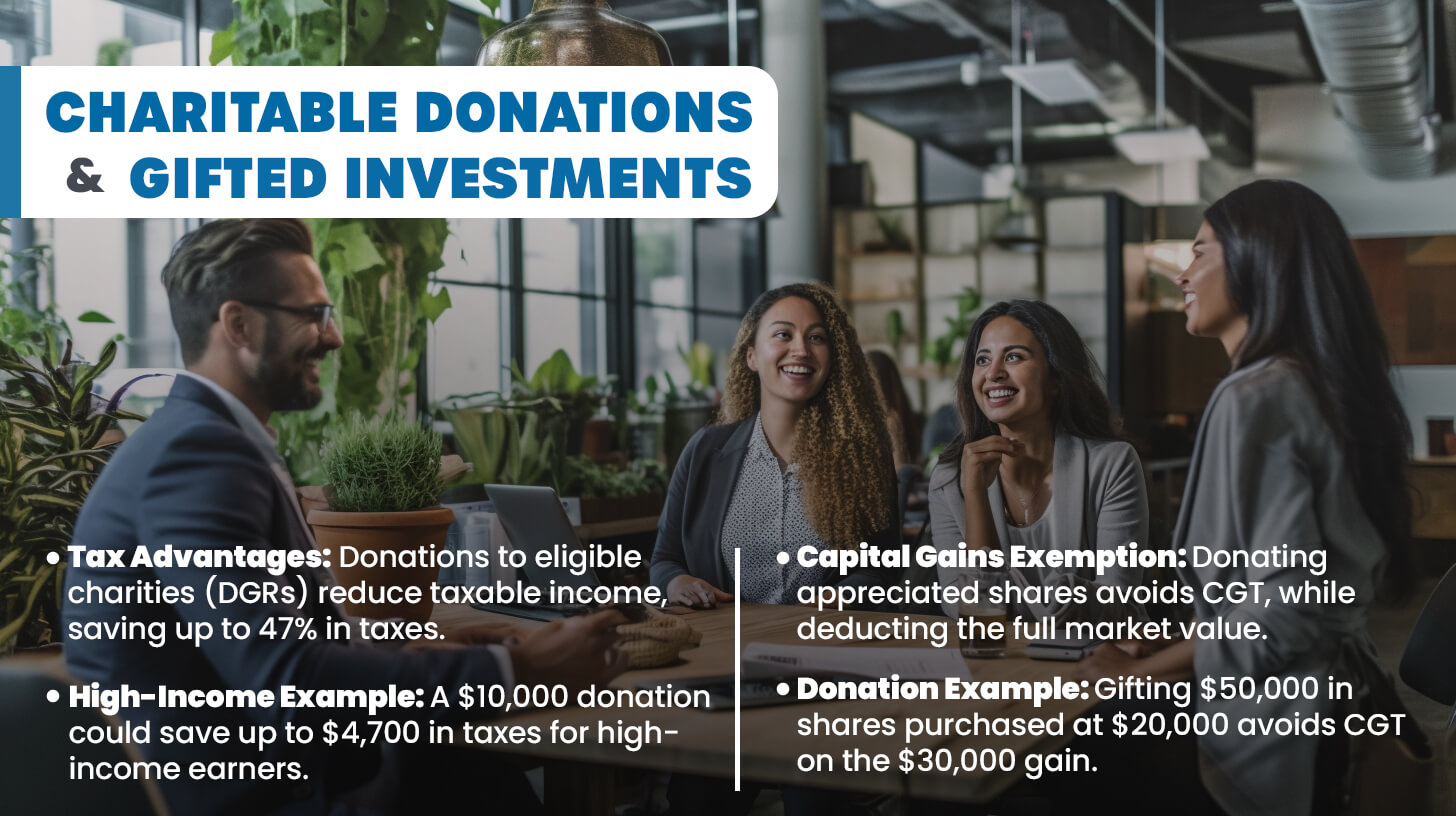

Charitable Donations and Gifted Investments

Charitable donations not only support causes that investors are passionate about but also offer substantial tax advantages.

According to Philanthropy Australia, charitable giving in Australia has grown steadily, with individual donations reaching over AUD 12.5 billion in 2022. Donations to eligible Deductible Gift Recipients (DGRs) are tax-deductible, reducing taxable income and, consequently, tax liabilities.

For instance, a high-income earner donating AUD 10,000 to a registered charity could save up to AUD 4,700 in taxes, assuming a top marginal tax rate of 47%. Beyond cash donations, gifting appreciated shares or property to DGRs can further enhance tax efficiency, as these assets are exempt from capital gains tax upon transfer.

An example of this is donating shares worth AUD 50,000 that were originally purchased for AUD 20,000. Instead of selling the shares and incurring CGT on the AUD 30,000 gain, transferring the shares directly to a charity allows the donor to avoid CGT altogether, while still receiving a tax deduction for the full market value of the shares.

This strategy turns charitable giving into a powerful tax management tool, combining philanthropy with financial prudence.

Charitable trusts and private ancillary funds (PAFs) further extend these benefits, allowing families and businesses to create structured giving plans that distribute funds tax-efficiently over time.

FAQ (Frequently Asked Questions)

What Types of Tax-Free Investments Are Available in Australia?

In Australia, various tax-free investment options cater to different investor needs.

One prominent choice is tax-free savings accounts, which allow individuals to save money without incurring tax on the interest earned. These accounts are often available through banks and credit unions, providing a secure environment for savings while optimizing returns.

Moreover, certain investment vehicles, such as tax-exempt managed funds, enable investors to accumulate wealth without tax liabilities.

Another compelling option is the investment in Australian real estate, particularly through primary residences. Homeowners can sell their properties without incurring capital gains tax (CGT), making property a favorable investment avenue.

Additionally, superannuation funds allow for tax-free earnings on investments held within them, particularly when in the pension phase.

As of 2023, the Australian Taxation Office (ATO) reported that approximately AUD 3.3 trillion was held in superannuation, highlighting the significant financial planning tool it represents.

How Do Tax-Free Savings Accounts Work in Australia?

Tax-free savings accounts in Australia offer a simple yet effective way for individuals to grow their wealth without incurring taxes on the interest earned.

These accounts function similarly to regular savings accounts but come with specific tax benefits. Interest accrued in these accounts is exempt from tax, allowing investors to maximize their returns.

Typically, these accounts are offered by various financial institutions, including banks and credit unions, with competitive interest rates.

For example, in 2022, the average interest rate for tax-free savings accounts was around 1.5%, appealing to many savers.

Furthermore, the Australian government promotes tax-free savings accounts as part of its broader economic strategy, encouraging citizens to save for their future.

By utilizing these accounts, individuals can accumulate wealth without the burden of tax liabilities, paving the way for a secure financial future.

Are Dividends from Australian Companies Ever Tax-Free?

Dividends from Australian companies can indeed be tax-free for certain investors, particularly those in lower tax brackets or retirees.

The franking credits system allows companies to pass on tax credits for the tax already paid on profits, which investors can utilize to offset their tax liabilities.

For instance, an investor receiving a fully franked dividend of AUD 1.00 may also receive a franking credit of AUD 0.30, effectively increasing their income to AUD 1.30.

If this investor is in a zero-tax bracket, they can claim a refund for the franking credits, resulting in tax-free income.

In 2021, the ATO reported that around AUD 35 billion in franking credits were claimed, demonstrating the significance of this mechanism in the Australian financial landscape.

Thus, dividends can serve as a robust income stream, especially for those strategically leveraging franking credits.

How Do Tax-Free Superannuation Contributions Work?

Tax-free superannuation contributions play a pivotal role in retirement planning in Australia.

Individuals can contribute to their superannuation funds from their pre-tax income, allowing for significant tax benefits.

The concessional contribution cap for the 2023 financial year is AUD 27,500, enabling individuals to contribute up to this limit while enjoying tax deductions on their taxable income.

For example, if an individual earning AUD 100,000 makes a concessional contribution of AUD 10,000, their taxable income is effectively reduced to AUD 90,000, resulting in lower overall tax liability.

Additionally, once in the pension phase, withdrawals from superannuation funds are tax-free, further enhancing the appeal of these contributions.

The ATO estimates that approximately 60% of individuals aged over 65 receive income from superannuation, emphasizing its importance as a source of retirement income.

Thus, tax-free contributions to superannuation not only foster retirement savings but also optimize overall tax efficiency.

Is the Income Earned from Certain Life Insurance Products Tax-Free in Australia?

Income earned from specific life insurance products in Australia can be tax-free, particularly in the context of investment-linked policies.

For instance, policies that combine life insurance with investment components often allow policyholders to accumulate capital gains without incurring tax liabilities.

When a policyholder receives a payout from a life insurance policy, the benefit is generally tax-free, provided the policy meets certain criteria set by the ATO.

As of 2023, it was estimated that over 50% of Australian households held some form of life insurance, highlighting the significance of this financial product.

Moreover, certain income protection policies offer tax-deductible premiums, making them an attractive option for individuals seeking financial security without incurring tax on the benefits received.

The nuances of tax treatment surrounding life insurance products underscore the importance of understanding how these financial instruments can fit into broader investment strategies.

How Does the Tax-Free Threshold for Investments Impact Returns in Australia?

The tax-free threshold in Australia significantly influences how investors approach their portfolios.

As of 2023, individuals can earn up to AUD 18,200 before incurring any income tax, allowing for strategic financial planning.

Investors can structure their income streams to remain within this threshold, maximizing their tax efficiency.

For example, a retiree receiving AUD 15,000 in investment income could strategically withdraw funds to stay under the tax-free limit, ensuring that their overall tax liability remains minimal.

This approach encourages a careful selection of investment products, with a focus on generating income that aligns with the tax-free threshold.

The ATO’s data shows that around 40% of taxpayers utilize this threshold effectively, showcasing its impact on overall investment returns.

Understanding how to navigate the tax-free threshold empowers investors to enhance their financial outcomes.

Can You Invest in Tax-Free ETFs in Australia?

Investing in tax-free exchange-traded funds (ETFs) is an appealing option for Australian investors looking to optimize their tax positions.

While no ETFs are completely tax-free, certain funds are structured to minimize tax liabilities, particularly those focusing on tax-efficient investment strategies.

For instance, ETFs that invest in Australian equities often come with franking credits, enhancing the effective yield for investors.

In 2022, the average dividend yield for Australian equity ETFs was around 4.5%, making them an attractive choice for income-focused investors.

Moreover, tax management strategies within these funds can lead to capital gains distributions that are minimized, allowing investors to benefit from potential growth without substantial tax impacts.

The popularity of tax-efficient ETFs has grown, with over AUD 60 billion invested in this asset class as of 2023, highlighting their significance in Australian portfolios.

Are Capital Gains from Property Investments Ever Tax-Free in Australia?

Capital gains from property investments can be tax-free in specific circumstances, particularly when it comes to primary residences.

Under Australian tax law, homeowners can sell their primary residences without incurring capital gains tax (CGT), provided they meet certain residency requirements.

In 2021, approximately 75% of property sales in Australia involved primary residences that qualified for this exemption, underscoring its importance for homeowners.

For investment properties, however, capital gains are generally taxable.

Nevertheless, if an investor holds the property for over 12 months, they may qualify for a 50% CGT discount, reducing the taxable gain significantly.

This discount encourages long-term investment strategies and enhances overall returns.

Understanding the nuances of capital gains tax is crucial for property investors aiming to maximize their returns while minimizing tax liabilities.

What Are the Benefits of Investing in Tax-Free Income Streams in Retirement?

Investing in tax-free income streams during retirement offers numerous advantages for Australian retirees.

The ability to receive tax-free income enhances financial security, allowing retirees to maintain their desired lifestyle without the burden of tax liabilities.

For instance, retirees accessing fully franked dividends from Australian companies can effectively utilize this income without worrying about taxes.

In 2022, it was reported that over 30% of retirees relied on tax-free income streams, showcasing their significance in retirement planning.

Moreover, tax-free income can be strategically managed to align with estate planning goals, ensuring that assets remain tax-efficient for beneficiaries.

By incorporating tax-free income streams into their retirement strategies, individuals can enhance their overall financial stability while preserving wealth for future generations.

How Does the Capital Gains Tax (CGT) Exemption Apply to Investments in Australia?

The Capital Gains Tax (CGT) exemption in Australia plays a crucial role in shaping investment strategies.

Specifically, the primary residence exemption allows homeowners to sell their homes without incurring CGT, a significant financial relief.

In 2021, the ATO reported that around 75% of homeowners sold properties without any CGT liability, benefiting from this exemption.

For investors, the CGT discount applies to assets held for more than 12 months, reducing taxable gains by 50% for individuals.

For instance, if an investor sells an investment property with a capital gain of AUD 200,000, they would only pay tax on AUD 100,000 if they meet the holding period requirement.

Understanding and navigating CGT exemptions is essential for investors seeking to optimize their tax obligations while maximizing returns.

Are There Any Tax-Free Investment Options for Children in Australia?

Tax-free investment options for children in Australia provide an excellent opportunity for long-term wealth accumulation.

Family trusts allow parents to set aside assets for their children while minimizing tax liabilities.

As of 2023, it’s estimated that over 1 million family trusts operate in Australia, underscoring their appeal in estate planning.

By allocating income to children, who may fall under the tax-free threshold, families can effectively manage their tax burdens.

Another option is educational savings plans, which allow parents to save for their children’s education while benefiting from tax-free growth.

In 2022, it was reported that over 30% of Australian parents were utilizing such plans, reflecting the growing awareness of tax-efficient savings strategies.

By leveraging tax-free investment options, families can secure a brighter financial future for their children.

How Do Franking Credits Impact Tax-Free Dividend Income in Australia?

Franking credits play a pivotal role in enhancing tax-free dividend income for Australian investors.

This system allows companies to pass on tax credits for the tax already paid on profits, effectively boosting the income investors receive from dividends.

For instance, if an investor receives a fully franked dividend of AUD 1.00, they may also receive a franking credit of AUD 0.30, increasing their income.

If this investor is in a low or zero tax bracket, they can claim a refund for the franking credits, resulting in tax-free income.

In 2021, the ATO reported that around AUD 35 billion in franking credits were claimed, illustrating the importance of this system in maximizing dividend income.

Understanding how franking credits operate enables investors to enhance their income streams while effectively managing tax obligations.

Are Any Renewable Energy Investments Tax-Free in Australia?

Renewable energy investments in Australia often come with favorable tax treatment, making them attractive to environmentally-conscious investors.

While not entirely tax-free, investments in renewable energy projects may qualify for various incentives, including tax offsets and grants.

The Australian government has committed significant resources to promote renewable energy, allocating AUD 1.5 billion in funding for initiatives aimed at increasing clean energy usage by 2030.

For instance, the Small-scale Renewable Energy Scheme (SRES) provides financial incentives for residential and small business solar energy installations, enhancing returns for investors.

Additionally, some investment funds focus exclusively on renewable energy, often structured to minimize tax liabilities, further attracting investors interested in sustainability.

The growing emphasis on renewable energy investments signifies a shift toward greener investment options, benefiting both the environment and investors alike.

What Are the Implications of Holding Tax-Free Investments Within a Self-Managed Super Fund (SMSF)?

Holding tax-free investments within a Self-Managed Super Fund (SMSF) has significant implications for Australian investors.

SMSFs provide control over investment choices, allowing members to tailor their portfolios to include tax-free assets.

For instance, investments in certain real estate or shares can generate income without incurring tax liabilities, especially when in the pension phase.

As of 2023, it is estimated that over 1 million Australians hold SMSFs, reflecting the popularity of this investment structure.

Moreover, SMSFs can benefit from a maximum tax rate of 15% on earnings, and this rate can drop to 0% in the pension phase, further enhancing tax efficiency.

By strategically managing investments within an SMSF, individuals can optimize their retirement savings while enjoying the benefits of tax-free income.

Are There Tax-Free Benefits for Investing in Australian Venture Capital Funds?

Investing in Australian venture capital funds presents unique tax-free benefits, primarily through the Early Stage Venture Capital Limited Partnership (ESVCLP) scheme.

This initiative offers significant tax incentives for investors, including a 10% non-refundable tax offset on contributions, fostering a vibrant startup ecosystem.

As of 2023, the ESVCLP framework has attracted over AUD 1 billion in investments, highlighting its appeal among investors looking to support innovation while enjoying tax benefits.

For example, an investor contributing AUD 100,000 to an ESVCLP could claim a tax offset of AUD 10,000, effectively reducing their taxable income.

Moreover, capital gains derived from these investments may be exempt from tax if held for the required period, enhancing overall returns.

Understanding the advantages of investing in venture capital funds empowers investors to support emerging businesses while optimizing their tax positions.

Do Any Philanthropic Investments or Charitable Trusts Offer Tax-Free Returns in Australia?

Philanthropic investments and charitable trusts in Australia provide unique opportunities for tax-free returns, especially for those interested in social impact.

Donations to registered charities often come with tax deductions, allowing individuals to reduce their taxable income while supporting causes they care about.

As of 2023, it is estimated that Australians donated over AUD 11 billion to charitable causes, highlighting the role of philanthropy in the financial landscape.

Moreover, charitable trusts can be structured to provide income to beneficiaries while offering tax benefits to the donor.

For example, a donor-advised fund allows individuals to make contributions and receive immediate tax deductions while directing grants to charities over time.

By combining philanthropy with investment strategies, individuals can achieve financial goals while making a positive impact on society.

What Are Tax-Free Investment Options Available for Non-Residents Investing in Australia?

Non-residents looking to invest in Australia can explore several tax-efficient options, though the landscape is nuanced.

Australian tax law stipulates that non-residents are generally subject to withholding tax on dividends and interest, which can be up to 30%.

However, tax treaties between Australia and various countries may reduce this rate, often to 15% or lower, depending on the agreement.

Investing in Australian real estate is another avenue for non-residents, though it’s essential to note that capital gains tax applies upon sale.

However, if non-residents invest through a Managed Investment Trust (MIT), they may benefit from tax exemptions on certain income types.

For instance, the MIT regime allows for tax flows that can effectively minimize tax burdens on income derived from residential property investments.

Moreover, certain Australian shares may be eligible for franking credits, though non-residents cannot claim these credits for refunds.

Nonetheless, they can still enjoy reduced withholding tax rates on fully franked dividends under specific circumstances.

Overall, while non-residents face certain tax liabilities, strategic investment choices and awareness of international tax treaties can help optimize returns while navigating the complexities of Australian tax law.

Are There Tax-Free Investment Options Linked to Social Impact or Community Development?

Investments linked to social impact and community development are gaining traction in Australia, with several tax-efficient options available.

Social impact bonds (SIBs) represent a groundbreaking approach, allowing investors to fund social programs with the potential for financial returns.

As of 2023, there are over 25 active SIBs in Australia, aimed at various social issues, including homelessness and mental health.

Investors in these bonds may receive returns tied to the success of the funded programs, often with the possibility of tax-free income.

For example, a SIB aimed at reducing recidivism could yield returns if measurable outcomes are achieved.

The Australian government has committed to investing AUD 100 million in social impact initiatives, underscoring the growing emphasis on combining financial performance with social objectives.

Moreover, community development financial institutions (CDFIs) offer investment opportunities focused on under-served communities.

These institutions provide capital to support local businesses and social enterprises, often with tax advantages for investors.

By aligning financial goals with social impact, these investment avenues not only enhance community welfare but also foster a sense of shared responsibility among investors.

How Can Tax-Free Withdrawals from Retirement Funds Be Maximized in Australia?

Maximizing tax-free withdrawals from retirement funds in Australia is a strategic endeavor that can significantly enhance retirement income.

The key lies in effectively transitioning to the pension phase of superannuation, where members can withdraw funds tax-free.

As of 2023, superannuation assets have reached an impressive AUD 3.3 trillion, highlighting the importance of effective withdrawal strategies.

To maximize tax-free withdrawals, individuals should ensure they have reached the preservation age, typically between 55 and 60, depending on their birth year.

Once in the pension phase, all withdrawals from superannuation funds are exempt from tax, allowing retirees to access their savings without financial penalties.

For example, a retiree with AUD 500,000 in superannuation could withdraw funds to meet living expenses without incurring tax liabilities.

Furthermore, utilizing the tax-free threshold strategically can enhance cash flow.

If a retiree has other sources of income, such as part-time work or investments, they can structure withdrawals to remain within the tax-free threshold, minimizing overall tax exposure.

This approach allows for greater flexibility in managing cash flow while preserving the longevity of their retirement savings.

Ultimately, understanding the nuances of superannuation withdrawals empowers Australians to optimize their retirement planning and secure a comfortable lifestyle.

Are There Specific Tax-Free Investment Incentives for Early-Stage Startups in Australia?

Australia offers specific tax-free investment incentives designed to stimulate early-stage startups, primarily through the Early Stage Innovation Company (ESIC) program.

Launched in 2016, the ESIC initiative provides investors with significant tax benefits, including a 20% non-refundable tax offset on eligible investments up to AUD 200,000 and a 10-year capital gains tax exemption.

As of 2023, the ESIC program has seen over AUD 1 billion in investments directed towards innovative startups, emphasizing its appeal in fostering entrepreneurship.

For instance, an investor contributing AUD 50,000 to an ESIC can receive a tax offset of AUD 10,000, effectively reducing their taxable income for the year.

Furthermore, if the investment appreciates and generates capital gains after a 12-month holding period, those gains can be exempt from CGT.

This dual benefit encourages long-term investment in startups, fostering innovation and economic growth.

Moreover, the ESIC framework encourages investment in diverse sectors, from technology to healthcare, promoting a vibrant startup ecosystem.

By strategically leveraging these incentives, investors not only enhance their tax efficiency but also contribute to the growth of groundbreaking ideas and businesses.

The Bottom Line

By leveraging these tax-effective vehicles, investors can leave a lasting impact on society while enjoying the financial advantages of strategic philanthropy, creating a legacy that benefits both their financial position and the wider community.

Originally Published: https://www.starinvestment.com.au/what-are-tax-free-investments-australia/

Comments

Post a Comment