20 of the Safest Investment Options in Australia

What Are the Safest Investment Options in Australia for Reliable Returns?

Government bonds are a cornerstone for conservative investors. They are backed by the Australian government, providing a fixed return, usually between 3-4%, with minimal risk of default. These bonds are ideal for preserving capital while ensuring steady, predictable income.

For those seeking even lower risk, term deposits present a secure option. With guaranteed returns over a fixed period—typically around 3%—these deposits are suited for short-term financial goals.

Superannuation funds are a long-term strategy, benefiting from tax incentives. Popular options like AustralianSuper and Hostplus offer growth and conservative mixes, depending on the investor’s preference.

Lastly, ETFs and REITs provide diversification, offering exposure to equities or real estate with lower fees and risk, making them attractive for cautious investors looking for stable, consistent growth.

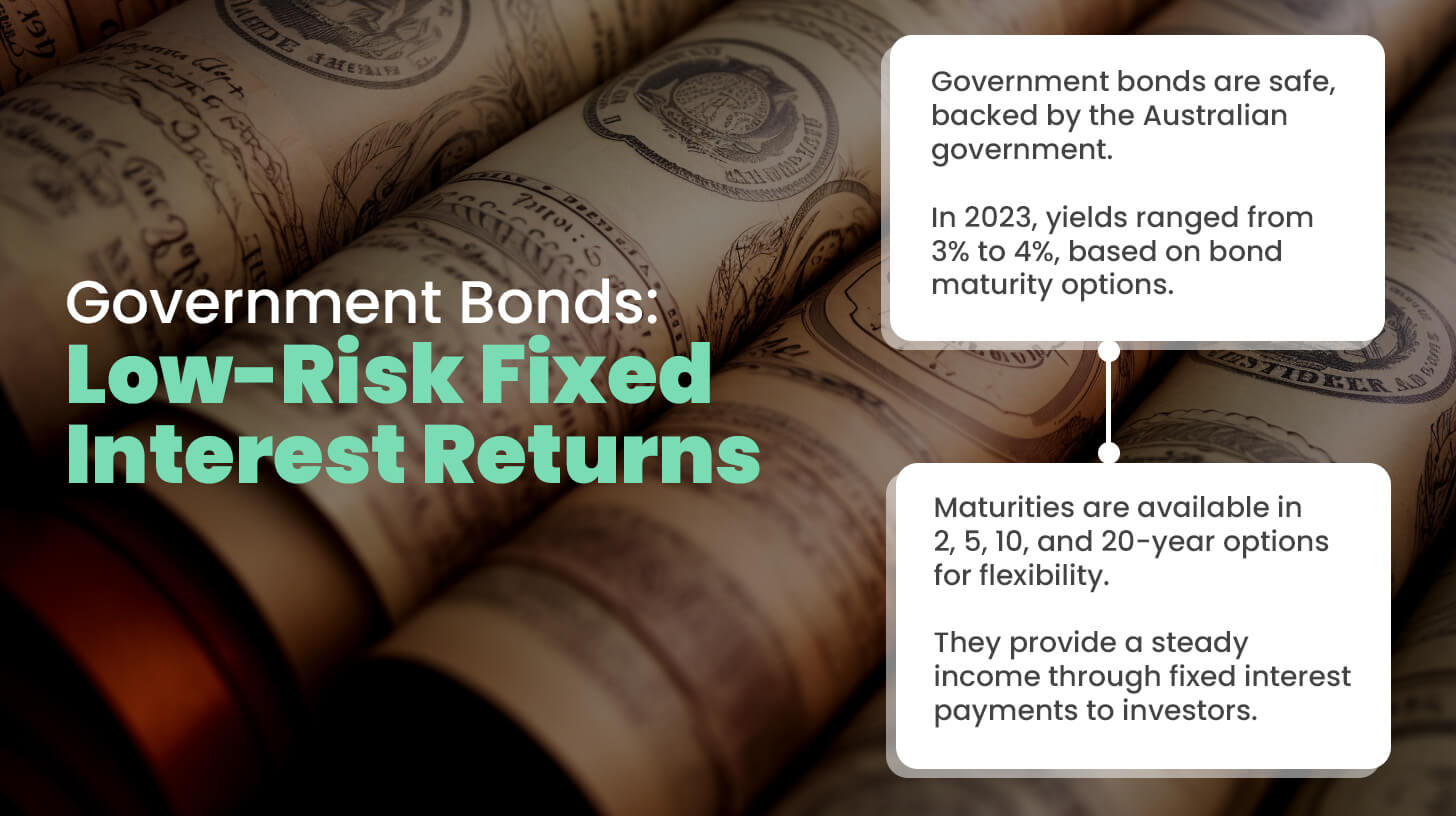

Government Bonds: Low-Risk Fixed Interest Returns

Government bonds are considered one of the safest investment options, as they are backed by the Australian government.

In 2023, Australian government bonds offered yields ranging from 3% to 4%, depending on the bond’s maturity. These bonds provide a steady income stream through fixed interest payments and are ideal for conservative investors seeking to preserve capital while earning a modest return.

Government bonds are typically issued for periods of 2, 5, 10, or 20 years, and investors can choose bonds with varying maturities depending on their financial goals.

They are also highly liquid, as they can be bought and sold on the secondary market. Given their low risk, government bonds are often used as a hedge during market volatility or as part of a diversified investment portfolio.

Corporate Bonds: Higher Returns with Moderate Risk

Corporate bonds, while riskier than government bonds, offer higher returns, making them a popular choice for investors seeking a balance between risk and reward.

In 2023, corporate bonds in Australia offered yields between 4% and 6%, depending on the issuing company’s creditworthiness. Corporate bonds are debt securities issued by companies to raise capital, and they typically pay higher interest than government bonds to compensate for the increased risk.

However, not all corporate bonds carry the same level of risk—investment-grade corporate bonds issued by financially stable companies offer lower yields but come with reduced risk compared to high-yield (or “junk”) bonds.

Corporate bonds are suitable for investors looking to diversify their fixed-income portfolios, with the added benefit of potential capital gains if the issuing company’s credit rating improves.

High-Interest Savings Accounts: Low-Risk, Competitive Returns

High-interest savings accounts offer a low-risk investment option with easy access to funds. In 2023, interest rates on Australian high-interest savings accounts ranged from 3.5% to 4.2%, depending on the bank and account terms.

These accounts are an excellent choice for conservative investors who prioritize liquidity while still earning interest. Examples of high-interest savings accounts include the AMP Saver Account and NAB Reward Saver, both of which offer competitive rates without requiring large minimum balances.

High-interest savings accounts are particularly attractive for those looking to preserve capital without exposure to market risks. Although the returns are modest, the safety and accessibility of these accounts make them an ideal short-term investment or a secure place to park emergency funds.

Term Deposits: Fixed Returns with Capital Protection

Term deposits are a secure investment option offering fixed interest over a set period. Australian term deposits in 2023 offered interest rates between 3.5% and 4.5%, depending on the term length and the financial institution.

The appeal of term deposits lies in their stability: investors know exactly how much interest they will earn, and their principal is protected for the duration of the term. Term lengths typically range from one month to five years, allowing investors to choose the duration that aligns with their financial goals.

While term deposits do not offer the flexibility of savings accounts—funds are locked in until maturity—investors benefit from guaranteed returns with no exposure to market volatility. Term deposits are particularly well-suited for risk-averse individuals or those looking for a secure way to grow their savings.

Real Estate Investment Trusts (REITs): Diversified Property Investment

Real Estate Investment Trusts (REITs) provide an accessible way to invest in a diversified portfolio of income-generating properties without the need to directly purchase and manage real estate.

In 2023, Australian REITs offered average dividend yields of 4% to 6%, making them attractive to income-seeking investors. REITs are publicly traded companies that own and manage commercial properties, such as office buildings, shopping centers, and apartment complexes. They generate income through rents and are required by law to distribute most of their earnings to shareholders in the form of dividends.

REITs offer liquidity, as they can be bought and sold like stocks on the ASX, and they provide diversification within the real estate sector. Investors can gain exposure to various property types and geographic regions, making REITs a popular choice for those looking to add real estate to their portfolios without the risks and challenges of direct property ownership.

Blue-Chip Stocks: Stable Companies with Reliable Dividends

Blue-chip stocks represent shares of large, financially sound companies with a long history of stable earnings and dividend payments.

In 2023, blue-chip stocks in Australia, such as BHP and Commonwealth Bank, provided dividend yields ranging from 4% to 6%, depending on market conditions. These companies are leaders in their industries and are known for their resilience during economic downturns.

Blue-chip stocks are ideal for investors seeking a combination of income and growth. While their share prices may fluctuate, their strong financial foundations and consistent dividend payments make them a reliable choice for conservative investors.

These stocks are also considered lower risk compared to smaller, more volatile companies, and they often form the cornerstone of a long-term investment portfolio focused on stability and gradual capital appreciation.

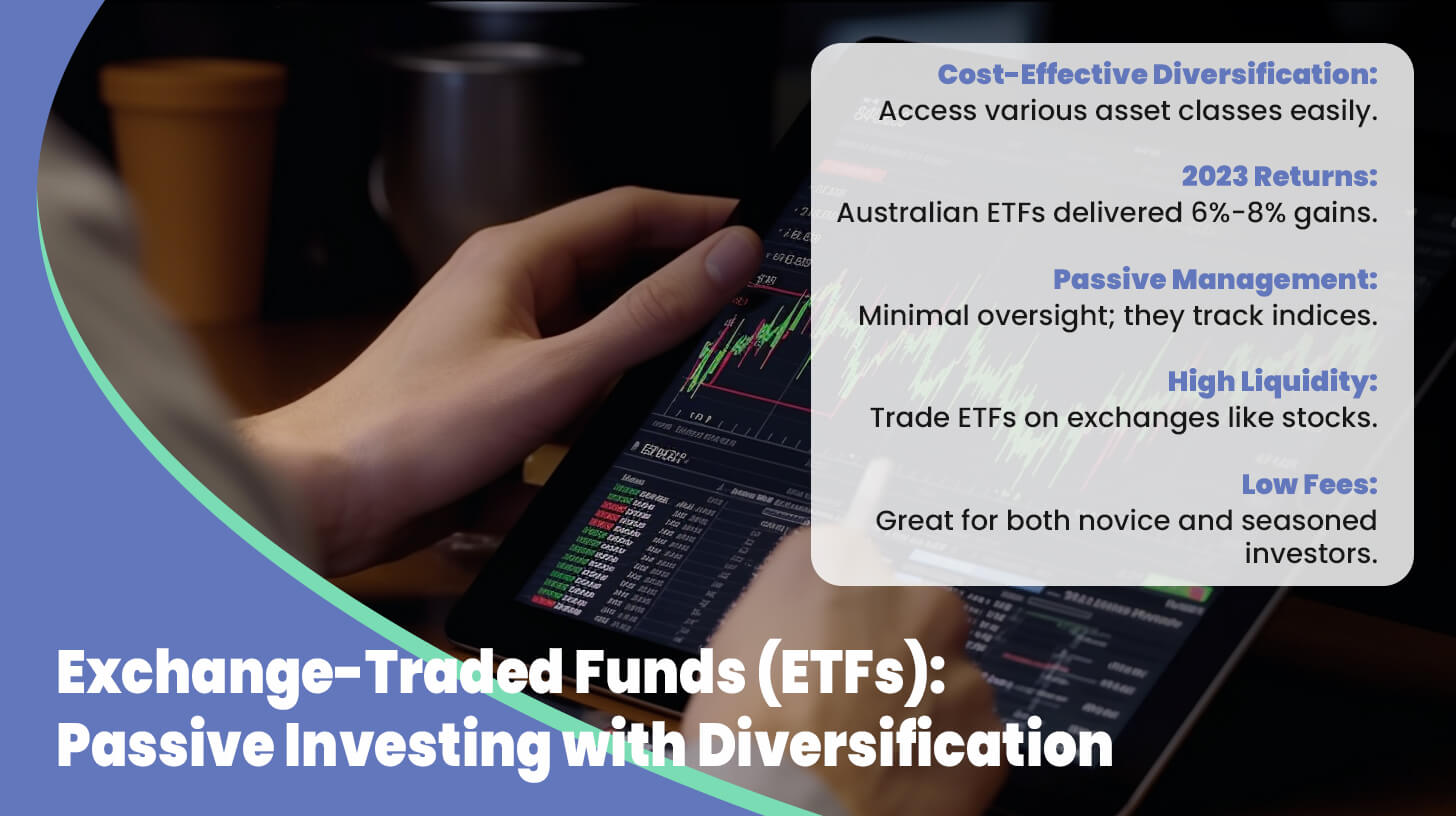

Exchange-Traded Funds (ETFs): Passive Investing with Diversification

Exchange-Traded Funds (ETFs) offer investors an easy and cost-effective way to achieve diversification across various asset classes, including equities, bonds, and commodities.

In 2023, Australian ETFs tracking market indices, such as the S&P/ASX 200, delivered returns between 6% and 8%, depending on the specific index and economic conditions. ETFs are particularly appealing for investors seeking passive management, as they typically track an index and require minimal active oversight.

ETFs also offer liquidity, as they can be traded on the stock exchange like individual stocks. This flexibility, combined with the low fees typically associated with ETFs, makes them an attractive option for both novice and experienced investors seeking broad market exposure.

Superannuation Funds: Mandatory Retirement Savings with Diversified Options

Superannuation funds are a compulsory retirement savings vehicle in Australia, offering a wide range of investment options tailored to individual risk preferences.

In 2023, balanced superannuation funds delivered returns between 7% and 9%, depending on the fund’s asset allocation and market performance. Superannuation funds are professionally managed and typically invest in a mix of shares, bonds, property, and cash, providing diversification and long-term growth potential.

Superannuation funds are ideal for long-term investors, particularly those focused on building wealth for retirement. The mandatory nature of superannuation ensures that Australians consistently contribute to their retirement savings, while the wide range of investment options allows individuals to tailor their portfolios based on their financial goals and risk tolerance.

Managed Funds: Professional Management with Diversified Assets

Managed funds offer a professionally managed investment option where a fund manager selects a diversified portfolio of assets on behalf of investors.

In 2023, Australian managed funds provided average returns ranging from 6% to 8%, depending on the fund’s strategy and market conditions. Managed funds can invest in a wide range of asset classes, including shares, bonds, and property, allowing investors to benefit from a diversified approach without the need to actively manage their investments.

These funds are suitable for investors seeking a hands-off approach, as they rely on the expertise of the fund manager to select investments that align with the fund’s objectives. Managed funds are also available in various risk levels, from conservative to high growth, making them a versatile option for a wide range of investors.

Investment Bonds: Tax-Efficient Long-Term Investments

Investment bonds are a tax-efficient long-term investment option that combines elements of both insurance and investment.

In 2023, investment bonds in Australia offered returns ranging from 4% to 6%, depending on the underlying assets and market conditions. These bonds are often used as a way to invest for the long term while deferring tax liabilities, as earnings within the bond are taxed at a lower rate than personal income if held for more than 10 years.

Investment bonds offer flexibility in terms of contribution amounts and investment choices, making them suitable for investors looking to accumulate wealth over time in a tax-effective manner. They are also popular for estate planning purposes, as they can be passed on to beneficiaries without probate.

Lifetime Annuities: Guaranteed Income for Retirees

Lifetime annuities provide guaranteed income for life, making them a popular choice for retirees seeking financial security.

In 2023, Australian lifetime annuities offered returns between 4% and 5%, depending on the provider and the terms of the annuity. These products allow retirees to convert a lump sum into a series of regular payments, which can be tailored to increase with inflation or continue for the lifetime of a spouse.

One of the key benefits of lifetime annuities is the certainty they provide, as they eliminate the risk of outliving one’s savings. Annuities are particularly popular among retirees who value financial security and want to ensure that their income will last throughout their retirement, regardless of market fluctuations.

While returns may not be as high as other investment options, the peace of mind and guaranteed income make lifetime annuities an attractive choice for those prioritizing stability.

Cash Management Accounts: Liquidity with Modest Interest

Cash management accounts (CMAs) are a low-risk investment option that combines the features of a savings account and a checking account, offering liquidity and modest interest rates.

In 2023, CMAs in Australia offered interest rates between 2.5% and 3.5%, depending on the provider. These accounts are ideal for investors who want to keep their funds accessible while still earning a return on their money. CMAs are often used by investors to park cash temporarily before deploying it into higher-return investments.

Given their liquidity and security, CMAs are a suitable option for risk-averse investors or those who need quick access to their funds. Although the returns are modest, the convenience and stability of cash management accounts make them a reliable short-term investment choice.

Dividend Stocks: Regular Income from Reliable Companies

Dividend stocks are shares of companies that regularly distribute a portion of their profits to shareholders in the form of dividends. These investments are attractive to income-focused investors who seek both regular payouts and potential capital appreciation.

In 2023, Australian dividend stocks from large companies such as Commonwealth Bank, Telstra, and Wesfarmers delivered dividend yields ranging from 4% to 7%. Dividend stocks are especially popular among retirees and conservative investors looking for consistent income without needing to sell their shares.

While dividend stocks carry market risk, companies that pay dividends tend to be financially stable and well-established, making them less volatile than growth stocks. Additionally, dividend payments can help cushion portfolio losses during market downturns, providing a reliable income stream in times of uncertainty.

Cash Investments: Liquidity and Stability with Minimal Risk

Cash investments, including savings accounts and cash management trusts, are among the safest ways to preserve capital while maintaining liquidity. These options typically offer low but stable returns and are best suited for short-term savings or as a safe haven during market volatility.

In 2023, cash investments in Australia offered interest rates between 2% and 3%, depending on the financial institution and the type of account. While these returns are modest compared to other investment vehicles, the security and ease of access to funds make cash investments ideal for risk-averse investors.

These investments are especially useful for emergency funds, short-term financial goals, or as part of a diversified portfolio aimed at minimizing risk. The key advantage of cash investments lies in their stability and the fact that principal is not subject to market fluctuations.

Peer-to-Peer Lending: Higher Returns with Moderate Risk

Peer-to-peer (P2P) lending platforms, such as Prospa and SocietyOne, allow investors to lend money directly to borrowers, often small businesses, in exchange for interest payments. P2P lending can provide higher returns than traditional savings accounts or bonds, though it comes with increased risk.

In 2023, Australian P2P lending platforms offered returns ranging from 6% to 10%, depending on the creditworthiness of the borrowers. P2P lending allows investors to diversify their portfolios by lending to multiple borrowers across different industries, which can help mitigate risk.

However, since P2P lending is not insured by the government, investors face the potential for default, meaning careful selection of borrowers is essential. For those willing to accept the associated risks, P2P lending offers a way to generate higher income in a relatively low-interest-rate environment.

Gold: A Hedge Against Inflation and Economic Uncertainty

Gold has long been considered a safe haven asset, particularly during times of inflation or economic uncertainty. Investors can gain exposure to gold through physical bullion, gold ETFs, or gold mining stocks.

In 2023, gold prices remained relatively stable, hovering around AUD 2,700 per ounce, as investors continued to view gold as a hedge against inflation and market volatility. Gold’s appeal lies in its ability to retain value over time, making it a popular choice for investors looking to diversify their portfolios and protect their wealth from inflationary pressures.

While gold does not provide income like stocks or bonds, its historical role as a store of value and a hedge against currency devaluation makes it a valuable addition to any portfolio seeking stability.

Listed Investment Companies (LICs): Diversified Exposure with Long-Term Focus

Listed Investment Companies (LICs) are closed-ended funds that trade on the ASX and provide investors with diversified exposure to a range of assets, including shares, bonds, and property.

In 2023, Australian LICs offered dividend yields ranging from 4% to 6%, making them attractive to income-seeking investors. LICs differ from traditional managed funds in that they are listed on the stock exchange, allowing investors to buy and sell shares in the company rather than directly owning the underlying assets.

LICs are well-suited for investors who prefer a long-term focus and are looking for steady income combined with potential capital growth. They also offer the benefits of professional management and diversification, which can help reduce risk.

Commodities: Diversified Investments in Physical Assets

Commodities, including gold, silver, oil, and agricultural products, offer a way to diversify investment portfolios by gaining exposure to physical assets. These investments are often seen as a hedge against inflation or currency fluctuations.

In 2023, commodity prices fluctuated depending on global demand, supply chain disruptions, and geopolitical events. For example, oil prices remained volatile, with Brent Crude trading between USD 80 and USD 100 per barrel, while agricultural commodities such as wheat and corn saw price increases due to supply constraints.

Investors can gain exposure to commodities through ETFs, futures contracts, or direct ownership of the physical assets. Commodities are generally more volatile than stocks or bonds but can provide diversification and act as a hedge during periods of economic instability.

Income-Generating Assets: Reliable Returns through Rental Properties or REITs

Income-generating assets, such as rental properties and dividend-paying REITs, offer investors consistent cash flow along with the potential for capital appreciation.

In 2023, Australian residential rental yields averaged between 3% and 5%, while REITs offered dividend yields ranging from 4% to 6%. These assets are particularly attractive to income-seeking investors who want regular payouts without the need to actively manage a business or portfolio.

Rental properties, while providing steady income, require maintenance, management, and occasionally dealing with vacancies or tenant issues. On the other hand, REITs allow investors to gain exposure to real estate without the headaches of property management, making them a more passive form of income generation.

International Shares: Global Diversification for Risk Mitigation

International shares provide investors with the opportunity to diversify their portfolios beyond the Australian market, reducing reliance on the domestic economy and increasing exposure to global growth.

In 2023, international shares, particularly those in the U.S. and Europe, delivered returns ranging from 8% to 12%, depending on the region and sector. Investing in international shares allows for participation in industries not heavily represented in Australia, such as technology, pharmaceuticals, and emerging markets.

International shares also help mitigate risks associated with economic downturns in any one country, as they offer exposure to different currencies, economies, and growth trajectories. For Australian investors, international shares can be accessed via ETFs, managed funds, or directly investing in foreign stocks.

FAQ (Frequently Asked Questions)

Why is investing beneficial for long-term financial growth?

Investing plays a crucial role in building wealth over time. Unlike saving, where the principal amount remains relatively stagnant, investments have the potential to grow through capital appreciation, interest, or dividends.

In Australia, a well-diversified investment portfolio can yield returns far greater than simply keeping money in a savings account. Over the long term, investments in the ASX 200, for example, have historically averaged annual returns of around 9.5%.

Inflation is another factor that makes investing essential for long-term growth. With the current inflation rate in Australia around 4%, simply saving money in a low-yield account means your purchasing power diminishes over time. Investments, on the other hand, tend to outpace inflation, preserving and growing your wealth.

Furthermore, the power of compounding cannot be understated. When you reinvest your earnings, you gain returns not only on the original investment but also on the accumulated earnings. This exponential growth is key to achieving long-term financial goals, such as funding retirement or purchasing property.

How does a high-yield savings account work?

A high-yield savings account offers a higher interest rate compared to traditional savings accounts, making it an attractive option for Australians looking to grow their cash reserves without taking on significant risk.

In 2024, Australian banks are offering rates between 4% and 5% for high-yield savings accounts, which is significantly higher than the national average for standard savings accounts. These accounts are typically offered by online banks or smaller financial institutions that have lower operating costs.

The interest earned is usually calculated daily and paid out monthly, which allows for steady growth. However, it’s important to note that many high-yield savings accounts come with certain restrictions. For example, you may need to maintain a minimum balance or limit the number of withdrawals per month to avoid losing the higher rate.

While high-yield savings accounts provide better returns than a traditional savings account, they still offer limited growth potential compared to long-term investments. However, they are ideal for short-term goals or emergency funds, offering liquidity and security without the volatility of the stock market.

What are the risks and rewards of investing in CDs?

Certificates of Deposit (CDs) are low-risk investment vehicles where you agree to lock in your money for a set period in exchange for a fixed interest rate. In Australia, CD terms typically range from six months to five years, with interest rates varying depending on the term length.

The primary reward of investing in CDs is the guaranteed return. Unlike stocks or bonds, the interest rate on a CD is fixed, meaning you know exactly how much you’ll earn over the term. In 2024, Australian CDs offer interest rates ranging from 3% to 4.5%, which is relatively stable compared to other investment options.

However, there are risks associated with investing in CDs. The main drawback is the lack of liquidity. If you need to withdraw your funds before the CD matures, you may face penalties or lose some of the accrued interest. Additionally, in a rising interest rate environment, locking your money into a fixed-rate CD could mean missing out on higher returns elsewhere.

CDs are best suited for risk-averse investors or those who need a predictable income stream over a short to medium time frame.

Why should retirees consider corporate bond funds?

Corporate bond funds are an appealing option for Australian retirees looking to generate steady income while preserving capital. These funds invest in bonds issued by companies, which typically offer higher yields than government bonds or savings accounts.

In 2024, Australian corporate bond funds have yielded between 4% and 6%, providing retirees with a reliable income stream. This is particularly attractive in a low-interest-rate environment, where traditional savings accounts may not generate enough returns to cover living expenses.

Corporate bond funds offer diversification, as they invest in a variety of bonds from different sectors and companies. This reduces the risk of default from any single company, making it a safer option for retirees compared to holding individual bonds.

However, corporate bond funds are not without risk. Bond prices can fluctuate due to changes in interest rates or the financial health of the issuing companies. Retirees should be aware that while corporate bonds are generally safer than stocks, they still carry some level of market risk.

For those seeking steady income with moderate risk, corporate bond funds provide an effective balance between capital preservation and income generation.

What makes dividend stock funds appealing to investors?

Dividend stock funds, which focus on companies that regularly distribute a portion of their earnings to shareholders, are a popular choice among Australian investors seeking both income and capital growth. These funds typically invest in blue-chip companies with a history of stable earnings and consistent dividend payments.

In 2024, Australian dividend stock funds have offered yields between 4% and 6%, making them an attractive option for income-focused investors. In addition to regular dividend payments, these funds also provide potential for capital appreciation, especially during periods of economic expansion.

One of the key benefits of dividend stock funds is their ability to generate income even during market downturns. While stock prices may fluctuate, many companies continue to pay dividends, providing a cushion for investors during volatile periods.

However, it’s important to remember that dividend payments are not guaranteed, and companies may reduce or eliminate dividends during tough economic times. Despite this, dividend stock funds remain a popular choice for Australian investors looking for a balance of income and growth.

Who should invest in value stock funds?

Value stock funds, which focus on investing in companies considered undervalued by the market, are ideal for Australian investors who prefer a long-term, patient approach to wealth accumulation. These funds target stocks that trade for less than their intrinsic value, often due to short-term issues, market overreactions, or broader economic downturns.

Historically, value stocks have delivered strong returns during economic recoveries. In Australia, many value stock funds invest in large, established companies that have temporarily fallen out of favor. These companies often have strong fundamentals, including healthy cash flow and consistent dividends, making them appealing to investors seeking steady, long-term growth.

As of 2024, the average return on Australian value stock funds over the past five years is around 7%, outperforming many growth-oriented funds during periods of market correction. While value stock funds can offer substantial returns, they are not without risk. Investors need to be prepared for periods of underperformance, especially in fast-rising bull markets where growth stocks tend to dominate.

For individuals with a long-term horizon, the potential for capital appreciation and dividend income makes value stock funds a worthwhile investment.

Why are small-cap stock funds considered high-growth investments?

Small-cap stock funds are often viewed as high-growth investments because they focus on companies with smaller market capitalizations, typically between AUD 500 million and AUD 2 billion. These smaller companies tend to have higher growth potential compared to large, established firms.

In Australia, small-cap funds have delivered strong returns, with some funds averaging over 15% annual growth over the past decade. The appeal of small-cap stock funds lies in their ability to outperform larger companies during periods of economic expansion. Many of these companies operate in niche markets or emerging industries, allowing for rapid growth.

Additionally, smaller companies are often more agile and can adapt quickly to market changes, giving them an edge over larger, more bureaucratic firms.

However, with high potential rewards come higher risks. Small-cap stocks are generally more volatile, meaning they can experience significant price swings in short periods. This volatility can be exacerbated during economic downturns, when smaller companies may struggle to access capital or manage costs.

Despite these risks, Australian investors with a higher risk tolerance and a long-term outlook often find small-cap stock funds an attractive option for diversifying their portfolios.

What are the benefits of REIT index funds?

Real Estate Investment Trust (REIT) index funds offer Australian investors exposure to the property market without the need to buy physical real estate. These funds pool money to invest in a diversified portfolio of income-generating properties, including commercial, residential, and industrial assets. REITs must distribute at least 90% of their taxable income as dividends, making them attractive for income-seeking investors.

In 2024, Australian REITs have provided yields between 4% and 6%, making them a solid choice for those seeking regular income. Additionally, REIT index funds offer diversification, reducing the risk associated with owning a single property. By spreading investments across different sectors and geographic regions, REIT index funds can mitigate some of the risks tied to property market fluctuations.

Moreover, REITs provide liquidity that direct property investments do not. Investors can buy and sell shares in REIT funds just as they would with any stock, making it easier to manage their exposure to the real estate market.

This combination of income potential, diversification, and liquidity makes REIT index funds a valuable addition to a diversified investment portfolio, particularly in Australia’s property-focused market.

Why is the S&P 500 index fund a good choice for beginners?

For Australian beginners, the S&P 500 index fund is an excellent entry point into global markets. The fund tracks the top 500 publicly traded companies in the United States, providing broad exposure to various industries.

As of 2024, the S&P 500 has delivered an average annual return of approximately 10% over the past 30 years, making it one of the most consistent performers in the investment world.

The primary advantage of the S&P 500 index fund is its simplicity and low cost. Index funds are passively managed, which means they typically have lower fees than actively managed funds. For beginners, this makes it an affordable way to gain exposure to the stock market without the complexity of picking individual stocks.

The S&P 500 also includes well-established companies, reducing the risk compared to investing in a single company or sector. Additionally, the global reach of many S&P 500 companies allows Australian investors to benefit from the growth of multinational corporations, providing geographical diversification.

This makes it an ideal option for those looking to build a solid foundation for their investment portfolio.

How do Nasdaq-100 index funds provide tech exposure?

Nasdaq-100 index funds are an appealing option for Australian investors seeking concentrated exposure to the technology sector. The index consists of 100 of the largest non-financial companies listed on the Nasdaq stock exchange, many of which are technology giants like Apple, Microsoft, and Alphabet.

In 2024, Nasdaq-100 funds have delivered strong returns, with some funds achieving annual growth rates exceeding 15%. This growth is driven by the continued expansion of the tech industry, which remains a dominant force in the global economy.

For Australians, investing in a Nasdaq-100 index fund offers a simple and efficient way to gain exposure to high-growth tech companies. These companies often lead innovation, creating new products and services that drive long-term growth.

However, it’s important to recognize the risks. Technology stocks can be more volatile than other sectors, especially during periods of market uncertainty or regulatory changes. Despite these risks, Nasdaq-100 funds provide an opportunity for investors who are willing to embrace higher volatility in exchange for potentially higher returns.

Investors should also be aware that the Nasdaq-100 is heavily weighted towards large-cap tech companies, which means its performance is closely tied to the fortunes of just a few dominant firms.

What are the risks of investing in rental housing?

Investing in rental housing is a popular strategy for Australian investors, particularly given the strength of the country’s property market. However, this investment comes with several risks that must be carefully considered.

One of the primary risks is market fluctuation. Property prices in Australia can be volatile, particularly in urban areas like Sydney and Melbourne, where housing prices have experienced rapid growth followed by sharp corrections. Additionally, rental yields may not always cover mortgage payments, especially in periods of low demand or rising interest rates.

Maintenance and upkeep costs are another significant factor. Owning a rental property requires ongoing expenses, such as repairs, insurance, and property management fees. These costs can eat into the profitability of the investment, particularly if the property remains vacant for extended periods.

Furthermore, changes in government regulations, such as new tenancy laws or increased property taxes, can impact the profitability of rental properties. In 2024, several Australian states have introduced stricter tenancy laws, which may affect landlords’ ability to raise rents or evict tenants.

For those considering rental housing as an investment, it’s crucial to weigh these risks against the potential for capital appreciation and rental income.

How do you assess risk tolerance before investing?

Assessing risk tolerance is a fundamental step for Australian investors before committing to any investment strategy. Risk tolerance refers to an individual’s ability to withstand losses in their investment portfolio without experiencing undue stress or panic.

There are several factors to consider when assessing risk tolerance. Age plays a crucial role; younger investors typically have a higher risk tolerance as they have more time to recover from market downturns. Conversely, older investors nearing retirement may prefer lower-risk investments to preserve their capital.

Financial goals and time horizon are also key factors. An investor saving for a short-term goal, such as a home deposit, may have a lower risk tolerance compared to someone saving for long-term retirement.

Investors can also use risk tolerance questionnaires or consult financial advisors to better understand their comfort level with market volatility. These tools consider various factors, including income, savings, and investment experience, to help determine an appropriate risk profile.

Ultimately, understanding risk tolerance helps Australian investors choose the right mix of assets, balancing the potential for growth with the ability to weather market fluctuations.

Why is time horizon important in investment decisions?

Time horizon is a critical factor in making investment decisions, as it determines how long an investor plans to hold onto their investments before needing access to their funds. In Australia, where market conditions can be unpredictable, having a clear understanding of your time horizon helps shape your investment strategy.

For short-term goals, such as buying a car or funding a vacation, lower-risk investments like bonds or high-yield savings accounts are often preferred. These provide stability and liquidity, ensuring that funds are available when needed.

Conversely, long-term goals like retirement allow for more aggressive investment strategies, such as investing in equities or property. Over time, these higher-risk investments tend to generate greater returns, despite short-term volatility. For instance, the ASX 200 has shown an average annual return of around 9.5% over the past 30 years, despite experiencing several market downturns.

In essence, the longer the time horizon, the more risk investors can afford to take, as they have more time to recover from potential market dips. Understanding this dynamic allows Australian investors to tailor their portfolios in a way that aligns with their financial objectives and timeframes.

How can investors balance risk and reward?

Balancing risk and reward is one of the most important aspects of investing. For Australian investors, the key is to find the right mix of assets that aligns with both their risk tolerance and financial goals.

One way to achieve this balance is through asset allocation. By diversifying investments across stocks, bonds, and other asset classes, investors can reduce the impact of any single asset’s poor performance on their overall portfolio. Younger investors might lean more heavily towards equities, which offer higher potential returns but come with greater risk.

Conversely, older investors nearing retirement might shift towards bonds and other fixed-income assets, which provide stability and lower risk.

Dollar-cost averaging is also a popular approach in Australia, where investors contribute a fixed amount regularly to their portfolio, regardless of market conditions. This helps reduce the emotional impact of market volatility and smooths out the purchase price of assets over time.

Ultimately, the key to balancing risk and reward lies in a disciplined approach, with a focus on long-term growth rather than short-term market movements.

Why is diversification key in managing investment risk?

Diversification is a cornerstone of risk management in Australia’s investment landscape. By spreading capital across multiple asset classes, sectors, and geographies, investors can reduce the impact of any single investment’s poor performance on their overall portfolio.

For example, an investor who holds a mix of Australian equities, international shares, and bonds is less exposed to the risks of a downturn in the Australian market. The Australian economy is heavily reliant on certain industries, such as mining and banking. While these sectors have been strong performers, they also come with higher sector-specific risks.

By diversifying into other industries, like healthcare or technology, investors can protect themselves from the cyclicality of the resources sector.

Additionally, diversifying across asset classes helps manage risk. Bonds, for instance, tend to perform better when equities are underperforming, providing a cushion during market downturns.

A diversified portfolio with a mix of equities, bonds, property, and cash can help smooth returns and reduce volatility, especially during uncertain economic times.

For Australian investors, diversification is critical in managing both domestic and international risks, ensuring a balanced portfolio that can weather market fluctuations while still achieving long-term growth.

How can investors benefit from market volatility?

Market volatility can present opportunities for Australian investors, despite the perceived risks. While price fluctuations can cause short-term stress, they also create buying opportunities for those with a long-term perspective. When markets experience sharp declines, high-quality stocks often become undervalued, allowing investors to purchase shares at a discount.

Historically, the Australian share market has rebounded from downturns, providing substantial returns for those who buy during periods of volatility. For example, during the COVID-19 pandemic, the ASX 200 dropped by over 30% in early 2020.

However, investors who took advantage of this downturn saw the market recover by over 50% in the following months. This illustrates how volatility, while intimidating, can lead to significant gains for patient investors.

Moreover, strategies like dollar-cost averaging allow investors to systematically buy into the market, reducing the emotional impact of volatility. By investing a fixed amount regularly, investors buy more shares when prices are low and fewer when prices are high, smoothing out the effects of market fluctuations.

Volatility can also lead to innovation and growth in certain sectors. For instance, the tech and healthcare sectors saw substantial growth during the pandemic, providing investors with substantial returns.

Thus, volatility, when managed strategically, can be an advantage rather than a disadvantage.

What should be considered when choosing an investment advisor?

Choosing the right investment advisor is crucial for Australian investors seeking professional guidance. One of the primary factors to consider is the advisor’s qualifications and experience. Advisors in Australia are required to hold an Australian Financial Services (AFS) license or be an authorized representative of an AFS licensee.

Investors should verify that their advisor has the necessary certifications and experience to offer sound financial advice. Transparency about fees is another key consideration.

Advisors typically charge fees based on a percentage of assets under management, a flat fee, or an hourly rate. Understanding these fees upfront can help avoid conflicts of interest, where the advisor might recommend products that benefit them financially but may not be in the client’s best interest.

In Australia, recent reforms have increased transparency around advisor fees, making it easier for investors to evaluate the cost of advice.

Additionally, it’s important to assess the advisor’s investment philosophy. Some advisors may focus on active management, while others might recommend a more passive, index-based approach. Understanding their strategy and how it aligns with your own risk tolerance and financial goals is crucial for a successful advisor-client relationship.

Ultimately, finding an advisor who listens, communicates clearly, and aligns with your financial objectives is key to achieving long-term investment success.

What makes long-term investments preferable in a volatile market?

Long-term investments are often seen as preferable in volatile markets due to their ability to smooth out short-term fluctuations and deliver consistent returns over time. In Australia, where the stock market can experience significant volatility due to global and local economic events, long-term investments allow investors to ride out temporary downturns and benefit from market recoveries.

One of the key reasons long-term investments work well in volatile markets is the power of compounding. Over time, reinvested earnings, dividends, and interest accumulate, leading to exponential growth in the value of an investment.

Additionally, long-term investors are less likely to make emotional decisions based on short-term market movements. In volatile markets, investors who react quickly to negative news often lock in losses, while those who stay the course tend to recover and even profit as the market rebounds.

For example, during the 2008 financial crisis, the Australian share market dropped significantly, but long-term investors who held onto their investments saw the market recover and grow in the following years.

By focusing on long-term goals, such as retirement, education, or wealth-building, Australian investors can avoid the pitfalls of market timing and take advantage of the overall upward trend in the market.

How does investing help prepare for retirement?

Investing plays a critical role in preparing for retirement, particularly in Australia, where life expectancy continues to rise. With people living longer, the need for a substantial retirement fund is more important than ever. Simply relying on superannuation or government pensions may not provide enough income to sustain a comfortable lifestyle in retirement.

Through a well-thought-out investment strategy, Australians can grow their retirement savings significantly. Investing in a diversified portfolio of equities, bonds, property, and other assets allows for capital growth over time, helping to build a larger nest egg.

The earlier one begins investing, the more time they have to benefit from the power of compounding, where earnings generate additional returns. For example, an individual who invests consistently over 30 years will have significantly more saved for retirement than someone who begins investing later in life.

Moreover, a balanced investment portfolio can provide regular income through dividends, interest payments, or rental income, which can supplement superannuation during retirement.

For those nearing retirement, shifting to a more conservative portfolio helps preserve capital while still generating enough returns to outpace inflation. Overall, investing is a crucial component of any retirement plan, ensuring that individuals can maintain their desired standard of living throughout their retirement years.

Originally Published: https://www.starinvestment.com.au/safest-investment-options-australia/

Comments

Post a Comment